Theft and War at the Bank of England

World War One was funded with theft

In early October, many Londoners are coming to terms with the idea that the summer is now over. The rain has returned, the days end far too quickly, and the climate change propaganda has subsided somewhat. Gone are the t-shirts and sunglasses, to be replaced by thick jumpers and raincoats. The laissez-faire summer evenings have been replaced by the dull monotony of the daily commute.

However, far beneath the city, in the vaults below the Bank of England, nothing has changed. Andrew Bailey is conducting his daily séance to summon Lenin whilst mixing a cauldron of unicorn blood, gypsy tears and the remaining limbs of his interns. He gazes into a crystal ball, pondering to himself: Is the Bank of England LGBTQ2S+ friendly enough? Am I promoting homsexuality enough in the workplace? Do our press releases need more rainbows? Perhaps double rainbows? Am I a “he/him” or an “it/xim?” Suddenly, a face appears in the crystal ball. It’s John Maynard Keynes! He seems somewhat inebriated (quelle surprise!), and doesn’t look pleased.

“Andrew! You’re the Governor of the Bank of England. Stop faffing about with that gypsy magick and go and defraud your fellow countrymen! You should be at the printing press!”

“I am sorry master. I did not mean to disappoint you. What would you have me do?”

“Alright, what I want you to do is to send a telegram to Dishy Rishi and tell him that war is good for GDP, CBDCs are tools for freedom, and that paedophilia shouldn’t be a crime.”

“Hmmm, I don’t think I can do the last one.”

“Well, whatever. Worth a shot.”

The 2% target

The Bank of England has a lot of weird stuff on its website, but the page explaining their policy of a 2% inflation target is one of the most bewildering. Below, I’ll translate some of the tosh that they felt complacent enough to post.

BoE: “Inflation is a measure of how much the prices of goods (such as food or televisions) and services (such as haircuts or train tickets) have gone up over time.”

Reality: This is the modern definition of inflation, and this definition has been corrupted to the core. To be more specific, this is a definition of price inflation, not monetary inflation. Not only this, but its a very selective definition (one could say that its deliberately deceptive) because it only includes goods and services, both of which are naturally deflationary anyway because society grows more efficient over time, not less efficient. Goods and services, over time, fall to the marginal cost of production.

BoE: “Each month, the Office for National Statistics (ONS) collect around 180,000 prices of about 700 items. They use this ‘shopping basket’ to work out the Consumer Prices Index (CPI).”

Reality: The ONS takes a largely arbitrary basket of goods and services, and assumes an inflation rate for the “average person”. Absolutely no consideration is made for people living in different parts of the country, different transport requirements, health requirements, etc. It might as well be voodoo. It doesn’t take into account any of the developments and human progress that might become obsoleted from appearing in GDP figures. Jeff Booth often highlights the example of the calculator app: calculators used to cost £9.99 from W H Smith’s and then fell to a price of £0.99 when dematerialised into the App Store, and are now free by default on all smartphones: calculators have completely disappeared from GDP statistics, and yet society has improved (literally immeasurably). So what is GDP really measuring when denominated in CPI terms?

BoE: “To keep inflation low and stable, the Government sets us an inflation target of 2%. This helps everyone plan for the future. If inflation is too high or it moves around a lot, it’s hard for businesses to set the right prices and for people to plan their spending.”

Reality: The BoE has absolutely no idea how to plan for the future, as evidenced by the fact that even with rigged, fake statistics, we’re nowhere near their 2% target. The audacity to declare themselves a stabilising force is obscene. What sort of society is more stable when the entire financial establishment has to guess and second guess what side of the bed Andrew Bailey is going to wake up on? It might be a good system for hedge fund billionaires like Crispin Odey, who can attend champagne receptions with the Chancellor before major budgets, but it doesn’t work for anyone else. The 20th century should have taught even the most illiterate student of history that the “fatal conceit” of central planning isn’t sustainable. We wouldn’t want a single authority dictating the price of televisions, potatoes and oil, so why would we accept a world where unelected bureaucrats dictate the price of money?

Assuming that the Bank of England were able to achieve a CPI of 2%, and that CPI were an honest metric without the aforementioned shortcomings, would a 2% inflation rate really help people plan for the future? It would certainly be more tolerable than a 40% inflation rate, but its nonsensical to argue that the price distortion resulting from monetary inflation makes it easier to plan for the future.

BoE: “But if inflation is too low, or negative, then some people may put off spending because they expect prices to fall. Although lower prices sounds like a good thing, if everybody reduced their spending then companies could fail and people might lose their jobs.”

Reality: This is one of the most pernicious lies of Keynesian ideology, and one that most economists accept without a second thought. There are several problems with this assertion. Firstly, the idea that saving should be punished to incentivise spending and stimulating the economy is insane: people should be allowed to plan for their futures without The Bank determining that they are being selfish and that their attitudes are systemically risky to the economy. Choosing not to spend money in order to plan for the future is a critical economic decision that everyone has to make in their lives, and to penalise those who delay gratification incentivises myopic materialism.

Secondly, it assumes (as central planners invariably do), that in a deflationary world people would simply choose not to ever part with their currency to buy goods and services. The fact that this is one of the main tenets of the BoE’s justification for such a policy demonstrates the extent to which they are arguing in bad faith — it doesn’t make any sense. In a historical context, one can actually examine various metrics for establishing “innovations per capita” throughout periods in which currencies have been less inflationary or even deflationary: in The Bitcoin Standard, Ammous makes the case that it was because of such phenomena that the British had so many breakthroughs during the late 1800s and experienced the industrial revolution.

The fearmongering tactic of saying that “people may lose their jobs” is an anathema. As any entrepreneur knows, it isn’t the absolute price of goods and services that determines a company’s profits, but the margin when comparing outputs relative to inputs.

A 3% target?

“Thou shalt not steal” is a brilliant moral code upon which to base a society, and one may hope that with our Judeo-Christian traditions, there would be at least some political motivation not to have theft baked every transaction we do. Instead, we see a plethora of inexplicable mental gymnastics as politicians and central bankers try to justify even more exploitation.

A 2% target doesn’t make for a stable society. If I hit someone around the head with a cricket bat once a year, and each year they lost 2% of their braincells, they wouldn’t thank me for the stability (or maybe, after a few years, they would). Now, a 3% target? Who would advocate for such a thing?

Someone like Paul “The Fax Machine” Krugman. Why? Why indeed. One theory is that by changing the target to make it closer to where US inflation already is, the Federal Reserve can pat themselves on the back.

Within the current context of the collective West experiencing a debt spiral (debt to GDP now stands at 100% in the UK, 124% in the US), some will heightened degrees of inflation are actually beneficial so as to prevent a sovereign default, but this doesn’t mean that you should want to actually own any of the devaluing debt-based fiat currency.

CPI is a fake metric anyway

Even the measuring stick for calculating inflation is completely corrupt. The Consumer Price Index, by its very nature, isn’t going to be a very useful measure of changing prices for things that people actually want. If you want Netflix and Shreddies, then inflation may not seem too problematic at 6%, but if you want to know how much you need to save buy a home, then the CPI is a completely pointless metric.

If the establishment truly cared about housing affordability, healthcare affordability, retirement affordability, education affordability, etc., then they wouldn’t remove all of these metrics from their headline inflation figures. CPI isn’t an inaccurate reflection of inflation insofar as it pertains to one’s goals and ambitions; CPI is a metric that tells you how much more money you need to be earning each year if you want to remain poor. If you want to buy a house, then the inflation rate that you should be concerned about has historically been far higher. For example, the average price of a house in the UK was £8,700, and in 2023 it is circa £280,000 (a 32x increase). Over the same time period The Bank estimates sterling only lost 90% of its value. A useful trick for deceitful statistics: if you wanted to buy a home your sterling didn’t lose 90% of its value, but 97%. The value of your fiat savings was redistributed to the asset-owning class.

The theft isn’t accidental

There are many who will say “Oh, but perhaps this was just an unforeseen consequence of coming off the gold standard. How could we have known this would happen? There’s no ill will here.”

I confess that I thought along much the same lines, until digging a little deeper, at which point it becomes abundantly clear that this fiat world we live in was manufactured to intentionally plunder entire nations in one fell swoop.

| A-Z Quotes")

John Maynard Keynes, racist paedophile (I wasn’t being hyperbolic in the intro) and founder of Keynesian economics, fully understood how the theft could be conducted, and championed those who put his insidious ideas into action.

Much has been made of the two world wars and the destruction that they wrought on society. Scholars and historians debate whether or not Britain should have entered the fray in the first place. 103 years after the war broke out, in 2017, uncovered archives from the Bank of England revealed just how unnecessary and unpopular the war truly was.

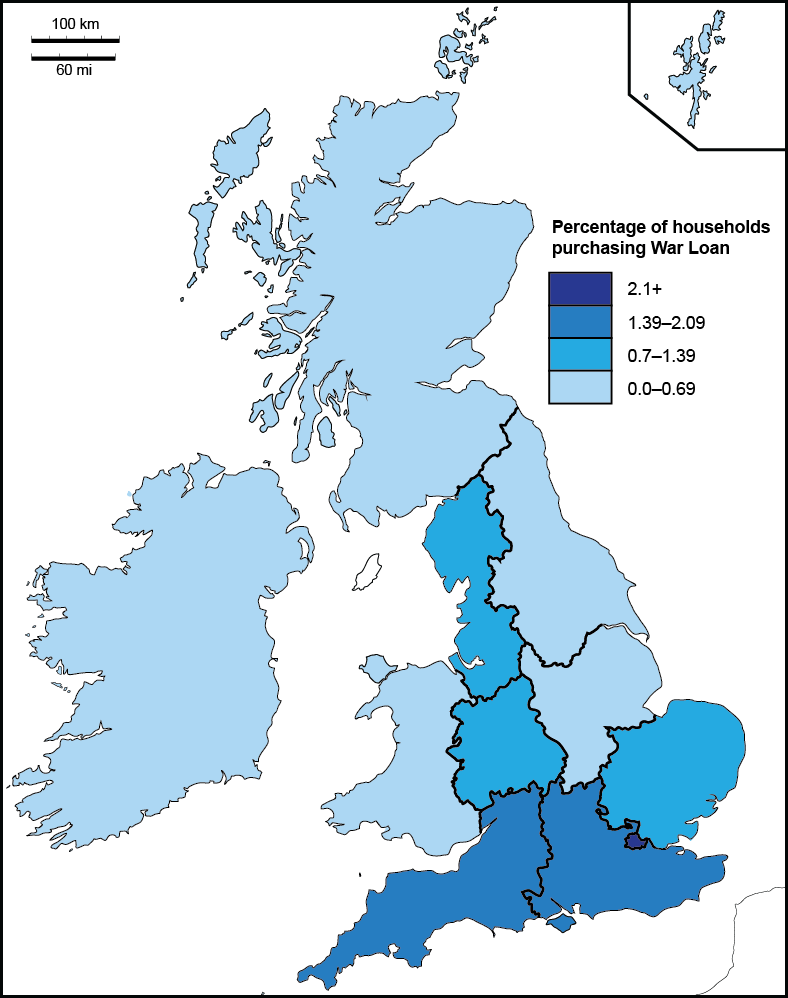

Before fiat, if a country wanted to wage a war then the state would need to raise funds in order to finance it. Often, citizens would choose to buy war bonds out of patriotic vigour, believing that the right thing to do would be to finance their government to kill foreigners. Others would choose to buy war bonds because they were concerned about external threats. In the case of World War One, that didn’t happen: the Bank of England issued war bonds, and hardly anyone bought them. Less than one third of the £350m target was raised. After all, what would we stand to gain by sending a load of 18 year olds to France to so that the King can flex his muscles in what was quintessentially a family dispute? At the time, government bonds were offering a yield of 2.5%, and the war bonds were being offered at 4.1% (showing that even the cunning and self-interested capitalist didn’t think war to be a worthwhile pursuit). The fact that they couldn’t sell nearly as much as they hoped was a disaster, and would have been a nightmare for public relations — Britons simply weren’t as war hungry as the establishment had hoped they might be.

However, rather than just simply not fight the war, the Bank of England decided to opt for a different strategy: conduct large scale fraud. The public would only learn about this deceit 103 years after the outbreak of the war, in 2017, when some employees went digging through old archives. Instead of admitting that the war wasn’t as popular as had been hoped, The Bank decided to plug the gap themselves, misappropriate depositors’ funds, and register the extra bond purchases under the names of the Chief Cashier and his deputy. A memo from 1915 was uncovered from Keynes to Treasury Secretary John Bradbury, where he shared how he believed it to have been a “masterful manipulation”.

On the 23rd November 2014, the Financial Times gushed that the war loan had been oversubscribed, and lamented that many Britons were going to miss out on being able to partake.

“There will be thousands of would-be subscribers to the War Loan disappointed of a really safe and — as “gilt-edged” securities go — profitable investment. What are they to do with their Capital now?”

In 2017, they issued an apology for deliberately misleading their readers.

Can we shut down the Bank of England?

If Guy Fawkes were alive today, I very much doubt that he’d bother with trying to blow up Parliament. If he really wanted to effect change in the 21st century, then it wouldn’t make sense to disturb the talking shop of corruption, chicanery and detachment that Westminster has become. Rather, it would be far better to dismantle the Bank of England, which is really at the root of the country’s problems. Without the hubris in Westminster that the BoE facilitates, the public sector might actually be forced to become efficient for a change; without access to the printing press, politicians would have no choice but to be fiscally responsible and put together budgets that actually mean something. If politicians didn’t have the ability to declare wars by diktat, and actually had to fundraise in order to wage them, we would have far fewer conflicts — citizens would weigh up the pros and cons of such a situation and choose whether or not they thought it worthwhile to finance, rather than being pillaged by their elected dictators.

Even if the coming decade doesn’t lead to hyperinflation of sterling (it very well may), doesn’t lead to having our freedoms stripped away with CBDCs (almost a dead cert), and doesn’t involve bail outs (or bail ins), we shouldn’t tolerate the theft that is so deeply entrenched in our currency. The Bank of England has used fiat to wage wars in the past, is doing so in the present, and will try to do in the future. All of these decisions are made without the feedback of the free market, and the mandate of citizens voting with their wallets. They do this without the consent or goodwill of Britons as a whole: by manipulating the currency itself, one can wage war on just about whoever they like for as long as they like, and for whatever reason. On a hard money standard, wars may be waged until it becomes impractical for the soldiers to do so, but on a fiat standard a war is waged until the entire nation becomes utterly impoverished. We have a moral imperative not to be complicit in this immorality: dump your sterling (dollars, yen, euros, roubles… its all the same), because if you don’t then The Bank will dump it on you when Bailey goes to the printing press. History shows us that central banks will resort to the printing press, and that one of the primary catalysts used to justify such a theft is usually war.

It’s 2023, and time for society to grow up: theft should be admonished whether it be for stealing a loaf of bread, looting a Morrison’s, or sapping the value out a nation’s savings. There’s no moral justification for breaking the seventh commandment, and its lamentable that doing so has become such an integral part of our world. A priori, one would conclude that a society without such a mechanism would be a better one, and that we shouldn’t lament the lack of nefarious tendrils that currently infest Britain’s financial hellscape. A posteriori, we can actually measure the impact of these policies, and the results are awful.

Pragmatically, a change as dramatic as closing the Bank of England would be radical when compared with the zeitgeist, and the shift would be uncomfortable. Fortunately, we do have alternatives: those open-minded enough to adopt the prerequisite weltanschauung to facilitate such a thing could be the drivers of a world that is far more peaceful.

An interesting addendum here from Jeff Booth's article "Finding Signal in a Noisy World":

"The existing fiat monetary system requires inflation and consequently, it needs manipulation to remain viable. We get less, for more work.

Because the existing system is credit based, it cannot allow ongoing deflation without complete collapse. (Because the credit would be wiped out and the credit IS the system) Society would never vote to have their entire way of living collapse. Which means a paradox exists where society will always eventually insist on manipulated “growth” for fear of the consequences of collapse, and that manipulated growth is the primary source of the problems that society is dealing with — including environmental damage.

Ultimately, this is because instead of allowing prices to fall (and society to gain time and freedom) with increasing productivity, it presupposes that we can “grow” forever. And the growth itself presupposes that money can be created out of thin air to achieve it. This “growth” for more jobs to be able to pay the bills, to pay for higher prices, which are manipulated higher in the first place keeps society on a hamster wheel unable to see that it is the system itself with its embedded growth obligation to service unrepayable debt that is responsible for all the pain. It gets worse, from the existing system every innovation lowering price or saving time in the future must be offset with more manipulation of currency to keep the existing monetary scheme going. Energy itself provides a good example. It is not like there hasn’t been an abundance of technology deployed into the exploration, production, transportation, and development of new energy sources. When you realize that the primary reason (increasing demand is important too) energy prices have risen against new energy coming online and efficiency gains of existing energy sources, is that they must rise to support the existing credit system, you also realize there is no way out from the system."