The UK Property Market is Collapsing

House prices have fallen 12% in the last 18 months when adjusted for inflation, and Lloyds estimates a 35% drop is possible by 2027

This article is a follow up to “Will the UK Property Market Collapse?”

The UK property market has been taking a hammering this year and house prices are falling at their fastest rate since 2009, with the average price of a home already having fallen by 5% thanks to a deadly combination of rising interest rates, a cost of living crisis, and a government that decided to blow the brains out of the economy in 2020. Now, Lloyds are preparing for a “worst case scenario” whereby the property market falls 35% by 2027, as demand continues to be curtailed and supply continues to increase.

According to Nationwide, house prices have fallen by 12% in the last 18 months when adjusted for inflation, painting an even bleaker picture.

One of the main reasons that so many people are eager to sell their homes is because they can no longer afford the mortgage repayments and don’t want to end up hostage to negative equity. Currently, there are 648,000 homes currently listed for sale, a 35% increase from 479,000 this time last year.

Moreover, with the rise in interest rates there has been a significant drop off in the number of people who are applying for mortgages. Amongst those who apply, there has been a decrease in the number of those who are approved.

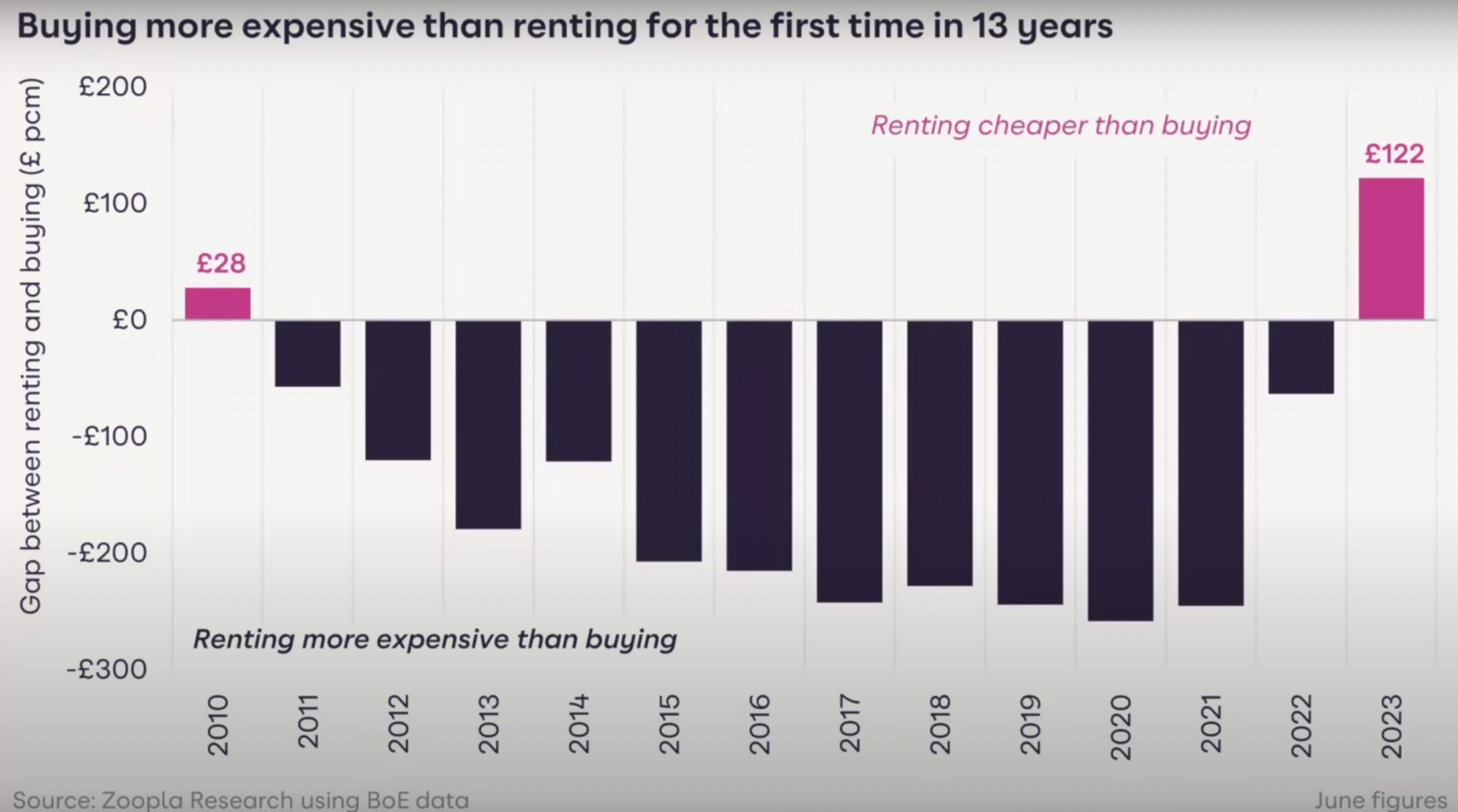

House prices versus earnings

One interesting data point is house prices relative to earnings. In a world that is growing more prosperous, one would expect this value to fall over time, as was the case before 1971.

In the late 1990s, average house prices reached a low of being worth only 3x average earnings, but this figure has ballooned to ~8x in 2022. In London, this figure is significantly worse, where the figure is over 12x (the Borough of Kensington and Chelsea standing at an impressive 38.4x).

Rising house prices are often seen as an indicator of a healthy economy, but such claims are heavily-laden with missing context. In general, one would hope that houses should become more affordable over time as a society becomes more prosperous, and that decreasing affordability isn’t something to be cherished but is actually symptomatic of rising inequality. In other words, rather than society becoming wealthier, a society’s wealth is simply redistributed.

In the US, the picture isn’t any brighter…

Buying versus renting

One of the main reasons that many people choose to buy a home in the first place isn’t just the psychological desire for shelter and sovereignty, but also that it has been the financially rational thing to do versus renting for much of history, thanks to the proliferation of mortgages whose interest rates are lower than the rate of monetary debasement.

This is yet another reason as to why demand has been curtailed so heavily.

When lockdowns were introduced, and remote work became more prevalent, so too did the exodus from cities to the countryside. Cities such as London, where home prices are significantly higher relative to wages compared with the countryside, may suffer the most from the coming decline. If Lloyds’ worst case scenario of a 35% decline nationally plays out, one shouldn’t be surprised to see London house prices falling by over 50%, and similarly large declines in the commercial real estate sector and the buy-to-let sector.

What could stabilise the housing market?

If inflation were to come down, the Bank of England would be able to once more lower interest rates to pump up the bubble once more. After all, when house price are denominated in fiat it shouldn’t be too hard for them to keep appreciating in relative terms: 80% of all US dollars in circulation were printed in the last three years alone, and its a similar story in the UK and the Eurozone.

One of the indicators that many believe to be particularly important is the relationship between wages and inflation. For the first time in months, UK wages have now risen once more above the CPI. Theoretically, this means that Britons should have more disposable income that could be used for housing. Realistically, the CPI is a stupid rigged metric designed for political purposes and serves absolutely no purpose whatsoever other than to facilitate and justify more government theft. Moreover, even if the CPI weren’t a load of complete tosh, the extra spending power wouldn’t be nearly enough to act as a counterbalance to the rises in interest rates.

The government (who are all homeowners with a stake in propping up the housing bubble), have sought to address some of the concerns that people have over housing affordability by creating even more subsidies to buy a house. According to Panorama, over 90% of the population has the desire to own their own home, which makes Britons ripe for having their dreams preyed upon.

The proposed solutions include — predictably — exacerbating inequality by inflating the bubble further. Every single UK political party is in lockstep as far as this goes. If the government really cared about making homes more affordable, then rather than simply increasing the price of homes relative to everything else, they would welcome a housing crash. The issue with this is that the state-sponsored encouragement of the housing bubble, predicated on the notion that “everyone should have the right to own their own home”, is detrimental to the social fabric as a whole and guts the middle class.

If these proposed solutions “succeed”, inequality will grow worse. If they fail, there’s a significant leg down before the market reaches an equilibrium once more. Top heavy societies, like boats, tend to topple. This scenario has already started to play out across China, where 60-75 million empty properties have been constructed with debt, and yet nobody lives in them. Now, Evergrande finds itself in over $340 billion of debt and the Chinese economy as a whole is tanking once more.

What do house prices really tell us about society?

The extreme financialisation of the housing market, and the fact that homes represent the majority of the average citizen’s wealth, can tell us a lot about the state of the economy and the society that we live in. The entrenched national psyche and its fixation with “getting on the property ladder” isn’t without cost.

We live in a world where the economic imperative is to become indebted in order to secure a rung on the ladder. Those who don’t do it are left behind as savings are debased relative to property prices, and those who do are left vulnerable to whatever crazy ill-informed tosh the Bank of England decides on any given day. The normalisation of mortgage debt is a cancer in society, especially when one considers how poorly-educated the hoi polloi are in financial matters, and how little they are aware of the potential risks. Debt isn’t something to be encouraged, but something to be cautious of. Currency should be a scarce store of value and medium of exchange, not a political weapon.

When the most basic foundations of Maslow’s hierarchy are financialised, perverse incentives are created whereby properties become assets rather than consumer goods. This means that the wealthy are incentivised to consume far more than they need, and a rewarded for doing so, whilst those without assets are punished. Moreover, wealthy property tycoons are able to take out collateralised LOCs against their properties with loans that aren’t marked to market — but for every second home or investment property purchased via such leverage, there is opportunity cost for the wider society. Nevertheless, when the asset class is politically preferred one doesn’t tend to see the diminishing marginal focus on property that would otherwise be rational.

When the money itself isn’t scarce, everything else becomes more so.

If only there were an asset that consisted of 100% monetary premium and could solve all of this…