The Halvening, High Wholecoiner Counts and Saucy On-Chain Analytics

Nothing is priced in.

With a hard cap of 21 million, there are only so many entities that will ever be able to own an entire Bitcoin, and this figure may be nearing its peak. According to Glassnode, the Bitcoin market experienced a 20% jump in wholecoiners in just one year, and there are now over one million wallets above this threshold. With the competition to become a wholecoiner heating up, the halvening around the corner, diminishing BTC supply on exchanges, and a wave of ETFs, the 2024-2025 market ought to be interesting.

Nearing peak wholecoiners

Theoretically, the absolute maximum number of wholecoiners that there could be is ~21 million, but this will never happen because there are far more people competing for Bitcoin and the supply is not distributed evenly (not to mention Satoshi’s coins and lost coins).

Realistically, there are likely far fewer than one million Bitcoiners who own an entire Bitcoin, given that each individual entity controls more than one address. There have been some estimates that the average Bitcoiner has in excess of 30 UTXOs; the one million milestone may therefore never truly be reached. Already, owning an entire BTC is out of reach for the majority of the world, and if the current trends continue then we may see the 1+ BTC cohort begin to top out and shrink.

2024 halvening dynamics

The halvenings every 210,000 blocks (roughly every four years) are one of the most important aspects of Bitcoin’s design to understand, since they undergird the entire industry.

Every halvening, the block reward is cut in half: the first halvening cut the block reward from 50 BTC to 25 BTC, then 12.5 BTC, then 6.25 BTC. In 2024, only 3.125 new BTC will be mined every 10 minutes.

![Next Bitcoin Halving 2024 Date & Countdown [BTC Clock]](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F81247679-187f-43e7-82d9-f668104095fb_1800x799.png "Next Bitcoin Halving 2024 Date & Countdown [BTC Clock]")

Cutting the inflation rate in half in such a way is extremely significant because it squeezes unprofitable miners and reduces selling pressure. It is thanks to the correlation between S2F and price that has spurred some of Bitcoin’s most famous price prediction models, such as Plan B’s.

With each cycle, one may predict that the effect of the halvening would diminish. After all, cutting the block reward from 50 to 25 is arguably more significant than cutting it from 6.25 to 3.125.

However, with these changes it may be more fruitful to compare BTC’s inflation with that of other asset classes. After the next halvening, Bitcoin’s inflation rate will fall to ~0.8%, making it the most scarce asset in the world (something that allocators ought to be aware of).

Spicy on-chain analytics

Although the effect of the halvening may diminish somewhat each cycle, there are new factors to consider this cycle. Most significantly, the total number of Bitcoin on exchanges continues to fall significantly, and this will be the first halvening where there are fewer Bitcoin on exchanges than at the previous halvening.

The chart below from Blockware Solutions demonstrates that from the Genesis Block to the first halvening, Bitcoin balances on exchanges rose to 2.18m. During the following halvening epochs this balance grew by a further 1.76m BTC and 1.26m BTC respectively. Although we are still several months away, the huge decline in Bitcoin on exchanges is sure to play a significant role. Since the last halvening, approximately 1.05m BTC have left exchanges.

The report from Blockware Intelligence goes on to suggest that this setup may incentivise larger players to participate in mining: if the current trend continues then by the early 2030s there’ll be more BTC yet to be mined than is available to buy on exchanges, meaning that large companies and nation states will be driven to mine if they want to accumulate large positions — either that or work directly for Bitcoin.

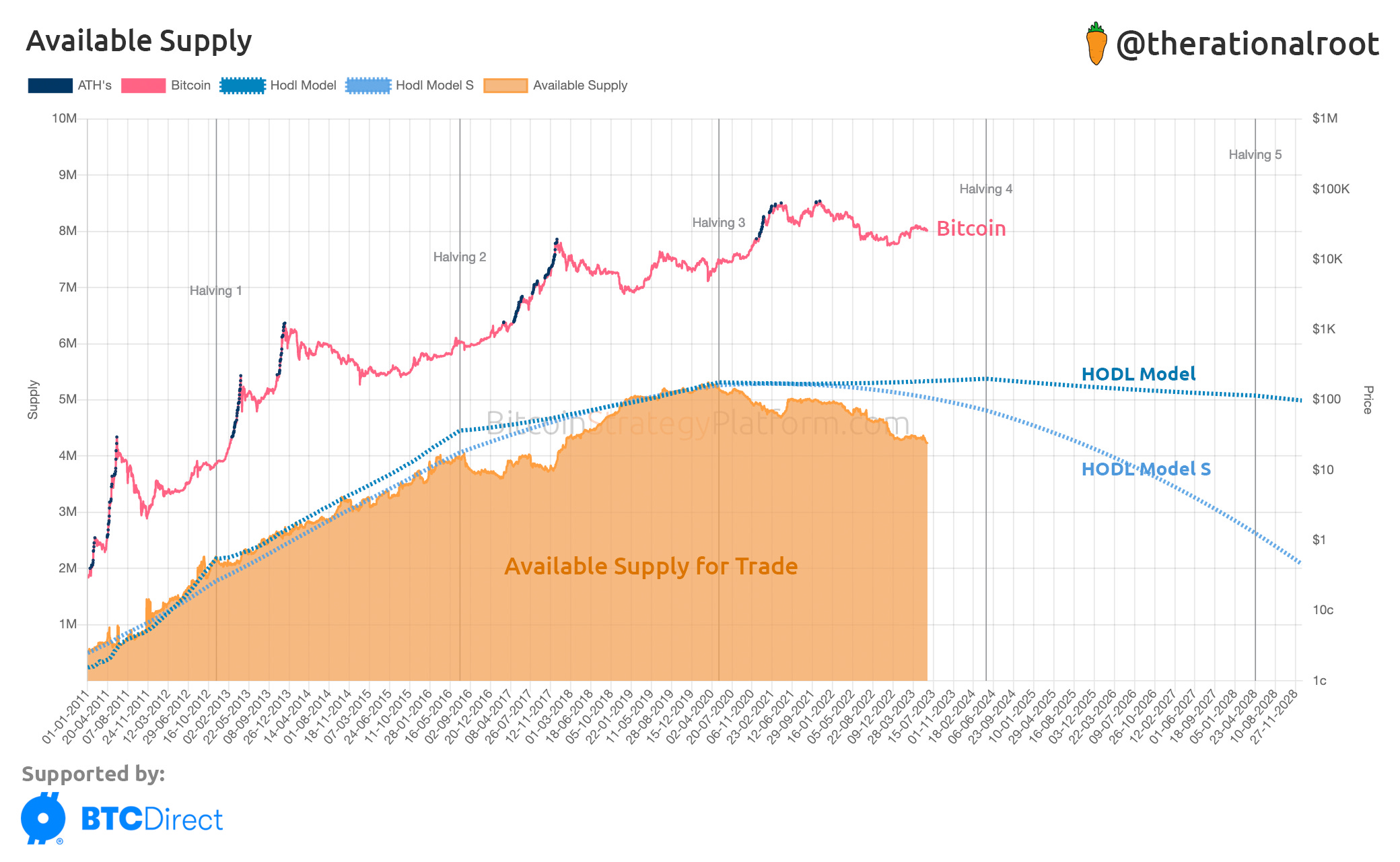

Root has argued that the theory of diminishing returns needs to be contextualised by taking into consideration the available supply of Bitcoin that is traded, and that the available supply of Bitcoin to be traded peaked in 2020, meaning that even though Bitcoin hit its ATH shortly after, it had to do so in the context of “BTC being the least scarce it had ever been”, and that “we haven’t yet truly seen what digital scarcity means.”

Other on-chain analysis has shown that more supply continues to get sucked up by the long term holders, and that this trend has continued despite the bear market. What this means is that over time a greater percentage of the Bitcoin network is owned by those who have the conviction and experience to weather the volatility, and that these holders are very insensitive to price changes. For the graphic below, long-term holders are defined as those who have held for at least two years.

ETF season

After the halvening, the catalyst that many are looking forward to in 2024 (although potentially this year) is the litany of ETF applications that have been submitted to the SEC.

Grayscale recently won a court case after the SEC rejected their last application, and the SEC’s protestations were thrown out by the court on the grounds that they were flimsy, and that their approval of Futures ETFs rather than Spot ETFs did not protect investors whatsoever. In fact, the Futures ETF has been harmful since it hasn’t managed to track the Bitcoin price very well anyway, most retail investors don’t understand Futures, and some investors instead ended up resorting tot he likes of SBF for exposure.

The markets rallied shortly after the court ruling and many were expecting the SEC to approve the seven other applications that have been filed by major firms almost immediately, but the SEC has delayed by another 45 days.

The first Bitcoin ETF application was filed by the Winklevoss twins in 2013, and had this been approved the US would likely be in a far better financial state than they are today. Nevertheless, it now seems as though the country’s incompetent regulators are being dragged into approval against their will. A BTC ETF would make it easy for retail investors to gradually build up their exposure through their ISAs and 401ks, and allow many of the largest funds in the world to gain BTC exposure without Grayscale’s extortionate fees (and inability to stay near NAV), and without concerning themselves with the custody dilemma.

Banking crisis not over yet?

The banking crisis this year has already meant that some of the world’s largest banks became insolvent and were bailed out. I was surprised by how little this was covered in non-financial news given the ramifications of the Fed’s BTFP programme, the Credit Suisse shenanigans, the distortion of incentives that were created, and the incredibly positive way that BTC reacted to the news.

According to Arthur Hayes, there is simply no way that the banking crisis is over, and that although many people feel somewhat reassured that they have been bailed out, there are still several banks who are functionally insolvent.

Some people have tried to make the case that all of this has been priced in. This is nonsense: 99% of people on Earth don’t even know what the halvening is. Most Bitcoiners are relatively unfamiliar with on-chain analysis, and I’d estimate single digit percentages in normie world can adequately explain what an ETF is. Whether a BTC ETF is approved this year, in 2024 or in 2025, Hector McNeil of HANetf has stated that the recent court ruling against the SEC demonstrates that a BTC ETF is now “just a matter of time”. Even amongst those who do understand all the above, many are not allocated accordingly: BTC currently represents ~0.1% of the world’s monetary mass, with investors like Greg Foss estimating that in the coming decade it could reach 5%. As supply continues to fall, demand continues to grow, obstacles for acquisition are removed, preexisting holders strengthen their conviction, and tradfi continues to collapse, the future for BTC is bright. Adam Back, founder of HashCash and CEO of Blockstream, is more bullish than ever and even made a bet that he believes BTC could eclipse $100k before the next halvening, given the larger macroeconomic context in which pressure is mounting on central banks to cut interest rates.